While the tech world is buzzing about Artificial General Intelligence (AGI), I’ve been diving into something different: IGI.

No, it’s not a new AI acronym. IGI stands for the International Gemological Institute, and they’ve recently gone public. Let me tell you why this company might just sparkle more than the diamonds they certify.

IGI caught my attention because of a simple yet profound investment principle popularized by Warren Buffett: invest in businesses so straightforward that even a monkey could run them.

Coca-Cola is a classic example. But did you know that this analogy once led to a bit of tension between Bill Gates and Coke’s CEO, Roberto Goizueta? At a public event, Gates mentioned the “monkey analogy” while Goizueta was on the stage with him —and, well, the two fellas never spoke again. Oops!

But back to IGI. Here’s why it’s a business that even a monkey could run:

Diamonds: The Universal Seal of Trust

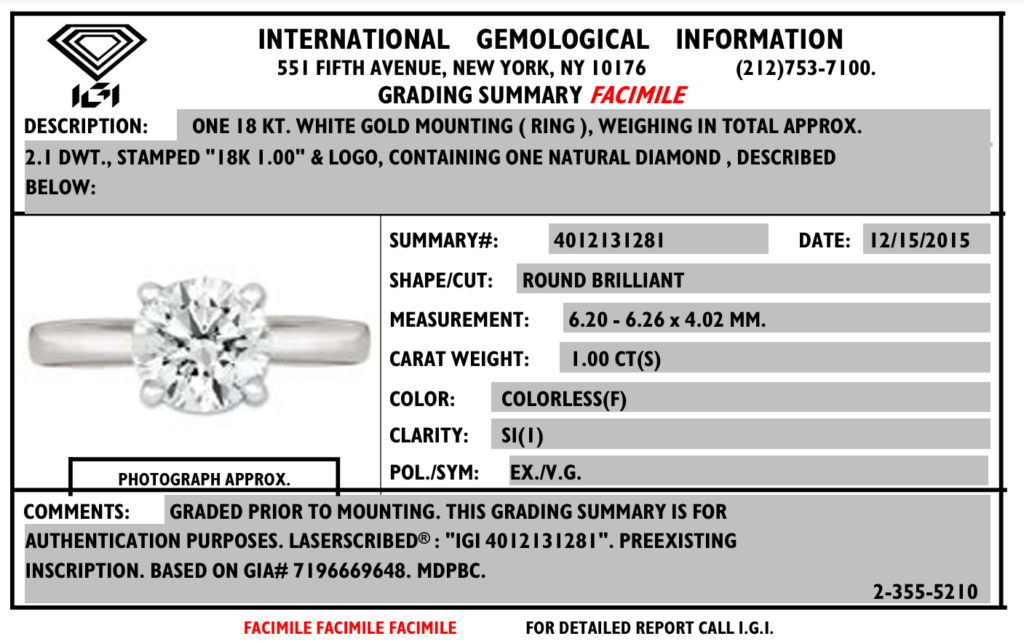

Have you ever purchased a diamond? Chances are, it was certified by IGI.

Diamonds are one of the most expensive commodities in the world, and no buyer wants to walk away without a trusted certification. That’s where IGI shines.

In May 2023, Blackstone acquired IGI for $530 million. Fast forward less than two years, and they’re taking it public at a valuation of $2.1 billion. That’s a 4x return in record time. Not too shabby.

So, is there still an opportunity for public investors? Let’s evaluate.

Blackstone though following the classic private equity playbook would still own 76% of the company after the IPO. Moreover, the Indian market regulator doesn’t allow promoters to exit the company for at-least 3 years after IPO, so we know for sure that Blackstone will own considerable equity in the company for the next 3 years.

The Duopoly: But better

What's better than a duopoly?

Duopoly with a non-profit!

The diamond certification market is essentially a two-player game:

- GIA (Gemological Institute of America): A non-profit.

- IGI (International Gemological Institute): A profit-driven powerhouse.

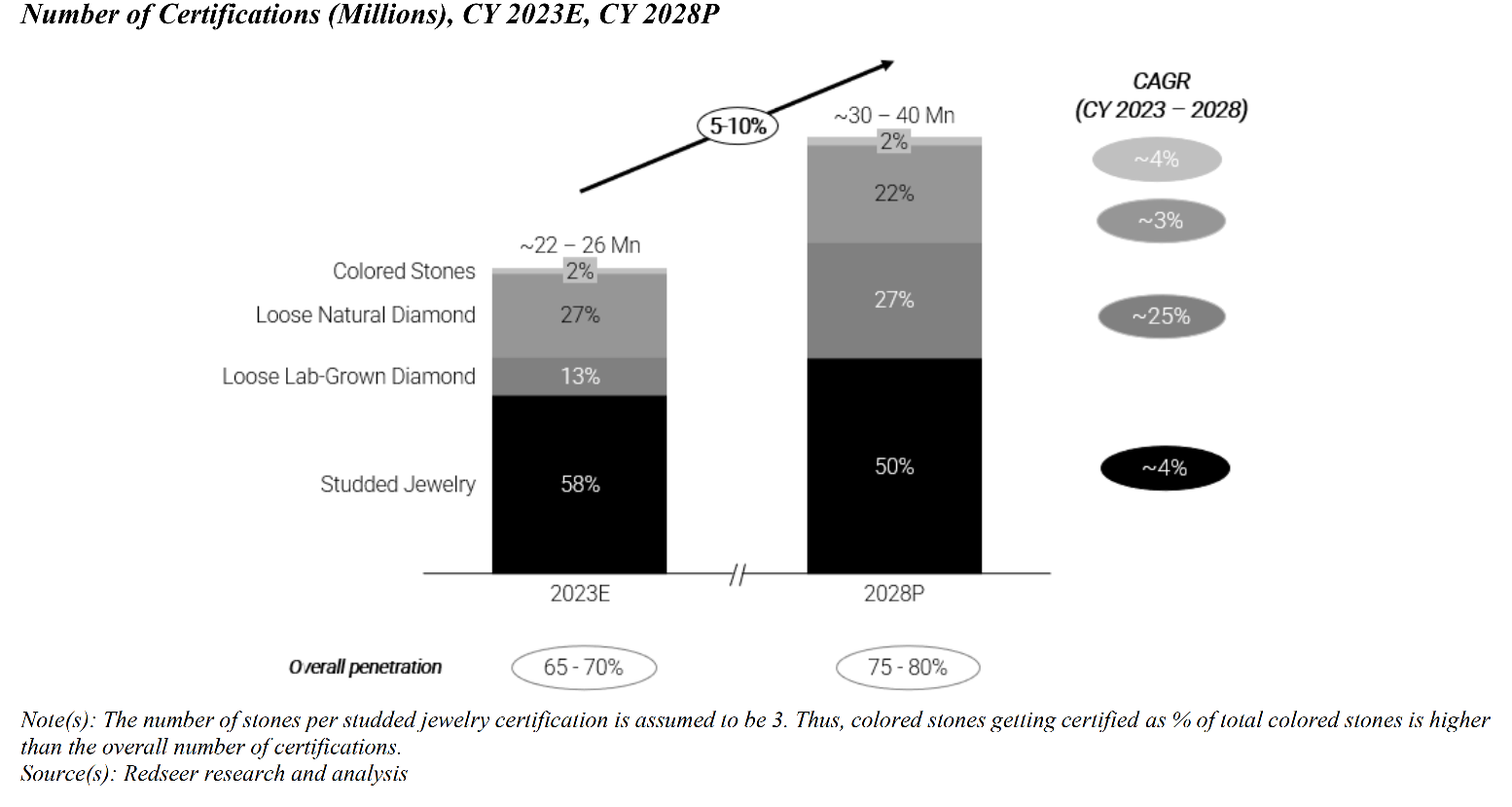

Overall in diamond certification, IGI has 33% market share.

GIA’s non-profit status is akin to OpenAI’s earlier days. Competing with profit-driven rivals while sticking to a non-profit model? Not easy. Just ask Sam Altman about OpenAI’s pivot.

IGI’s Glittering Moat

What makes IGI’s business model so robust? Three key factors:

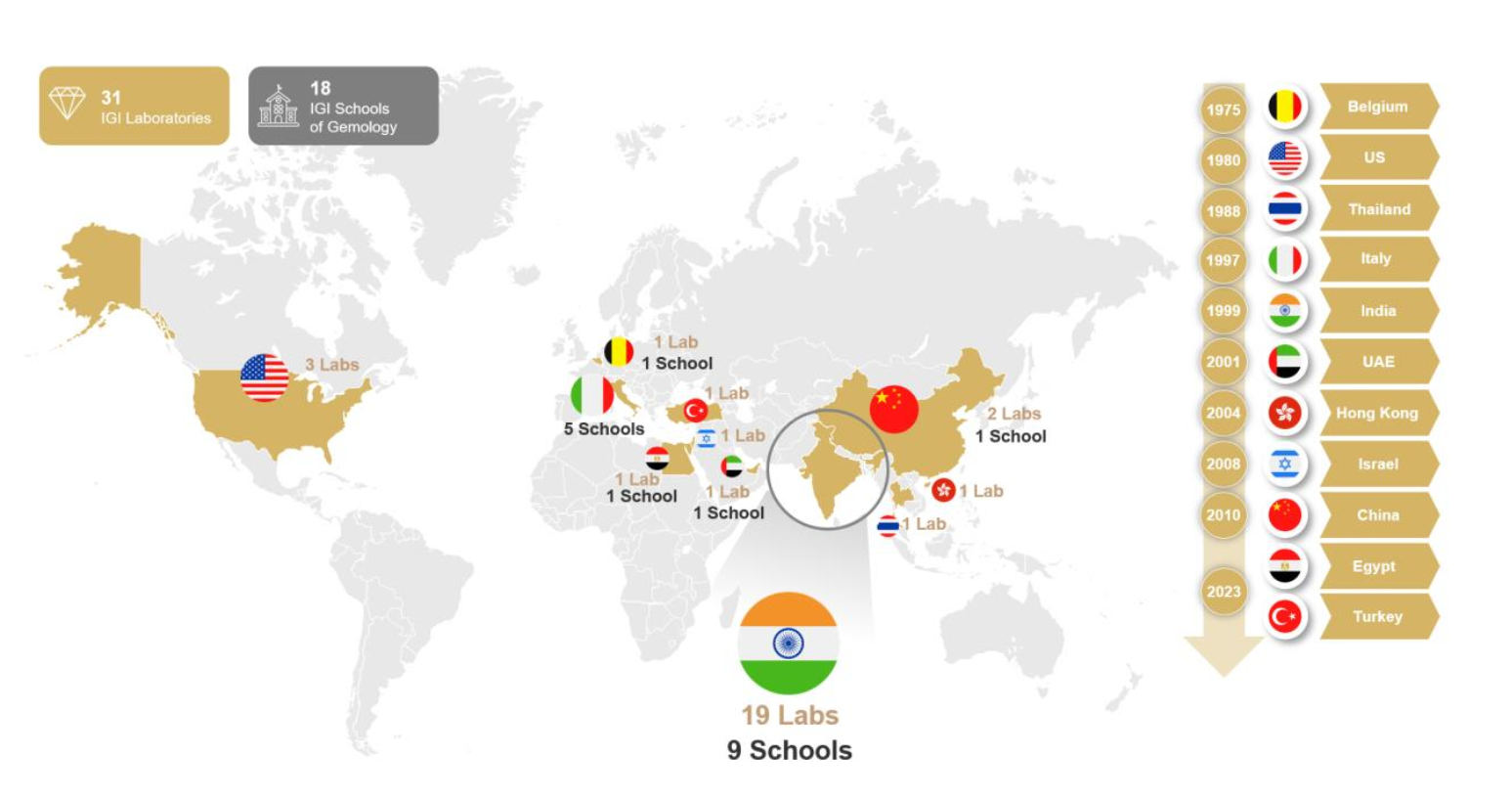

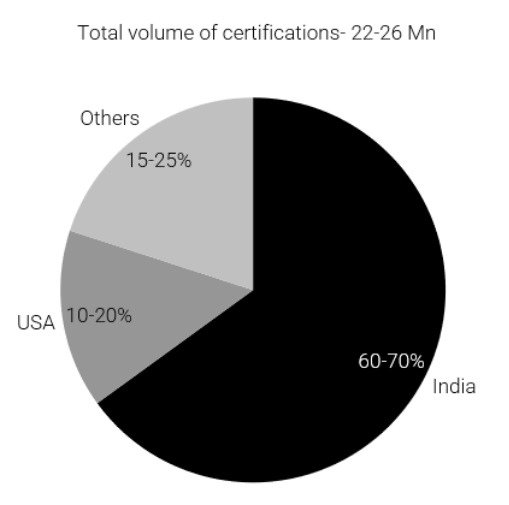

- Strategic Location: About 95% of the world’s diamonds are cut and polished in India. The best time to certify a diamond? Right after it’s cut and polished.

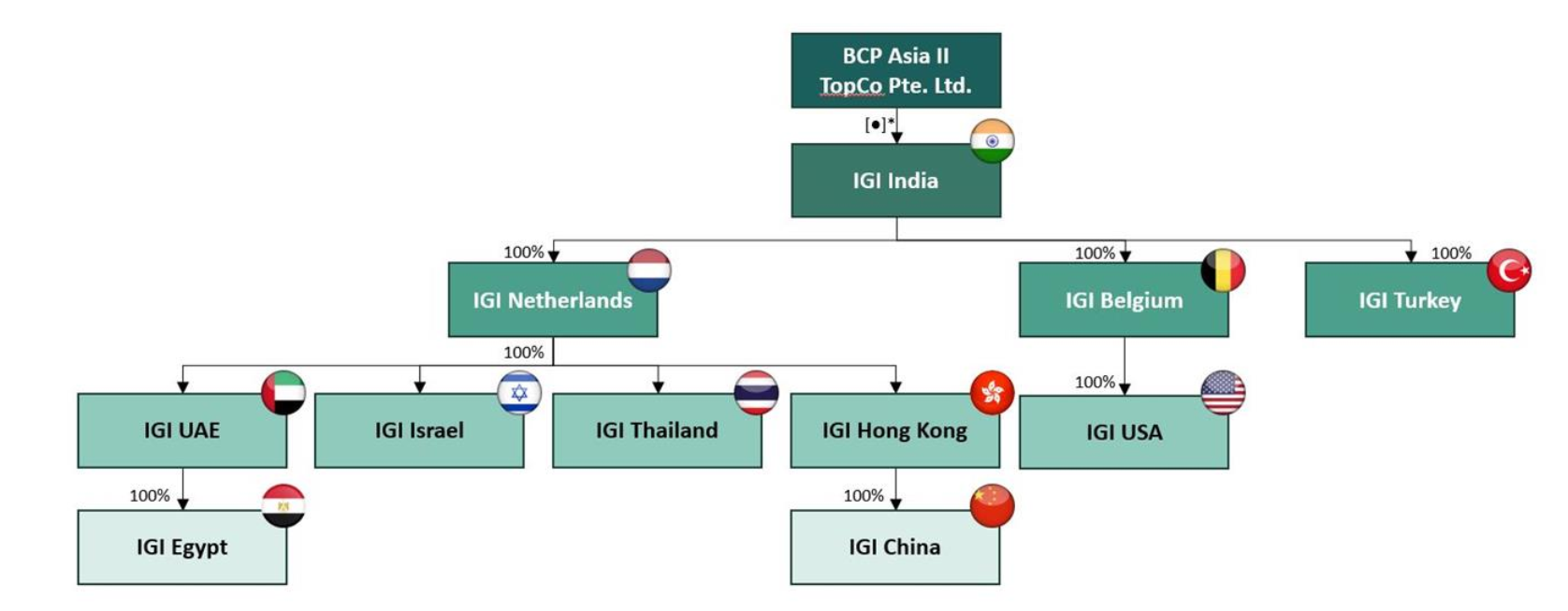

IGI, founded in Belgium in 1975, will officially be merged with IGI India along with IGI Netherlands, and move its global headquarters to India post-IPO. By situating itself where the action is, IGI ensures it’s always at the heart of the diamond trade.

IGI has not only the highest number of labs across the world, but also schools to train the next generation of gemologists.

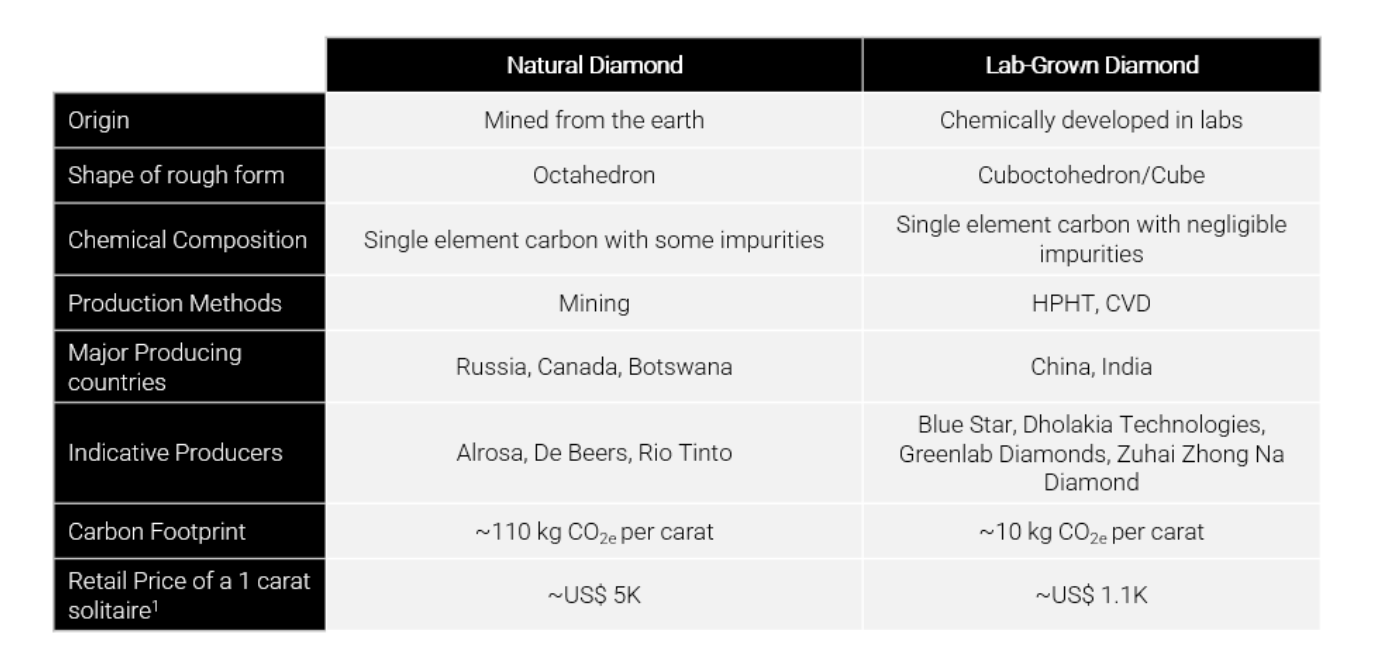

- Lab-Grown Diamonds (LGD): These are the future. With growing awareness around environmental, social, and governance (ESG) issues—not to mention movies like Blood Diamond highlighting the darker side of natural diamonds—LGDs are gaining traction. They’re physically, chemically, and optically identical to natural diamonds but cost only a fifth as much.

IGI dominates LGD market with a 65% global share, and the LGD market is growing at 15% annually—far outpacing the 1% growth of natural diamonds. Not to mention 35% of world’s natural diamonds are mined in Russia, which are under heavy sanctions after the Ukraine war.

Pandora in the US is strictly only selling LGDs.

- Low Gemologist Turnover: IGI has 316 gemologists working across 20 labs with an avg. tenure of 6.24 years! For comparison, average tenure in technology companies is only 1-3 years.

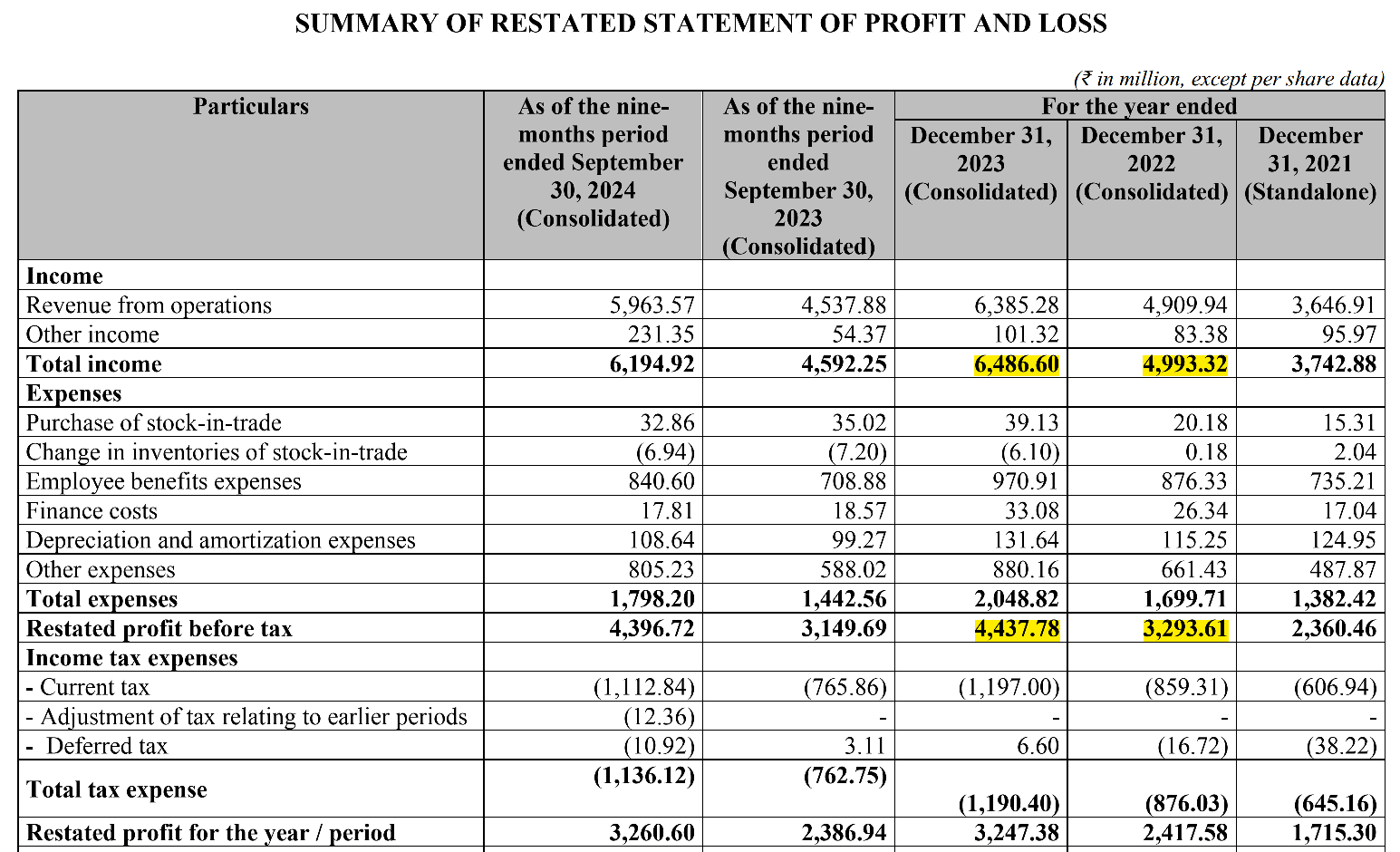

Financial Brilliance

Let’s talk numbers:

- Revenue growth: Over 30% year-on-year for the past few years.

- EBITDA margin: A dazzling 70%, higher than even giants like Visa and Mastercard.

- P/E ratio: ~55 (on the higher end). If you consider the projected growth rate in certifications and your investment time horizon is 2-5 years, this can workout just fine albeit there’s room for correction in pricing in the short term.

Risks

On paper, IGI looks like a great business. The biggest risk here is the valuation. At 55 P/E, there is no margin of safety for investors, but given the growth and duopoly in the diamond certification business one can argue it is justified.

Other major risk is the technology advancements in lab grown diamonds (LGD) production to the extent that certification is no longer necessary. Unlikely, but I’d assign a probability of 10% of it happening. On the flip side, I’d argue the more new entrants enter the LGD manufacturing space, the more people would want to see a seal of certification from IGI. It may put pressure on the margins, but will grow the top-line in tandem.

Why IGI Matters

IGI isn’t just a company; it’s an integral part of a global industry built on trust. As consumer preferences shift toward more sustainable and ethical options, IGI is perfectly positioned to capitalize on these trends.

In an era where many investors are chasing the next big tech breakthrough, IGI reminds me that there’s still immense value in businesses that meet timeless human needs—like trust and quality.

So, while others debate the future of AGI, I’ll keep an eye on IGI. Because sometimes, the best investments are the ones that shine right under our noses!

Get freshly brewed hot takes on Product and Investing directly to your inbox!