Nvidia’s stock recently took a 20% hit following the DeepSeek announcement, only to bounce back after Meta, Google, and Amazon made massive CapEx commitments. The AI boom is still in full swing, and Nvidia remains the dominant player.

Naturally, people have been asking: Is this a buying opportunity? Should I Buy, Sell, or Hold?

My Take

- If you’re an opportunistic investor looking for short-term gains, a trade could make sense. At least for the next 3-4 quarters, the spending would continue on Nvidia hardware. I’d actually bet that the stock could be another 10-15% higher after the earnings release on Feb 26. But the more important question to me really is – is this sustainable?

- If you’re a long-term investor, like myself, the volatility and opportunity cost are too high—I’m staying away.

The Problem: Nvidia’s Valuation Is Stretched

Most investors rely on the Price-to-Earnings (P/E) ratio to gauge a stock’s valuation. But here’s the issue:

📉 P/E assumes Nvidia’s profit margins will remain constant.

That’s a dangerous assumption.

I believe Nvidia’s margins will shrink in the future, and when that happens, the stock price could take a significant hit.

Let’s do some Napkin Math:

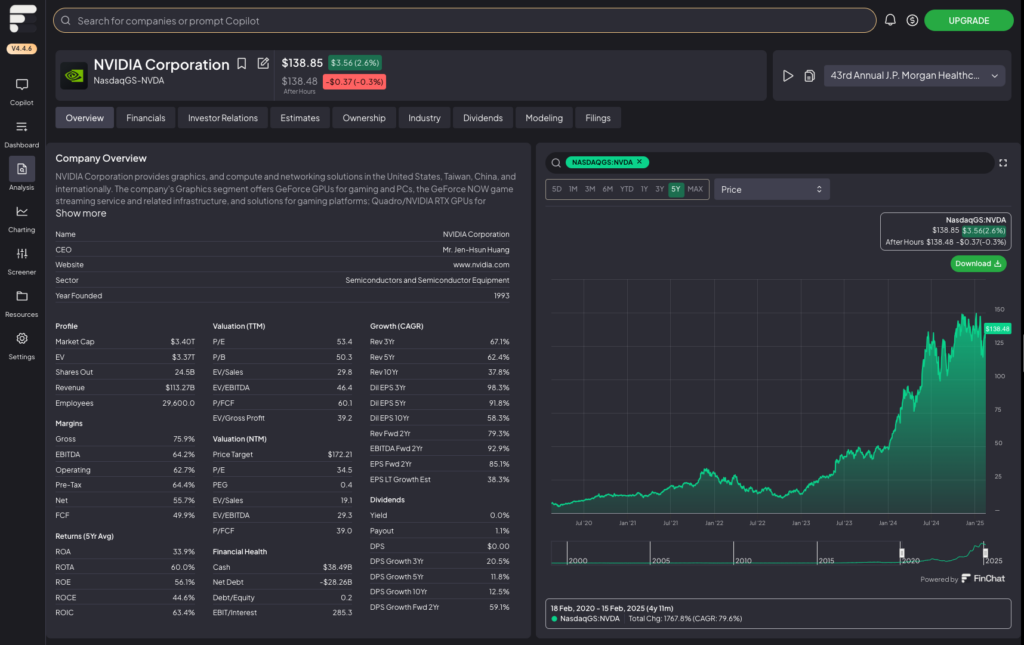

At a share price of $140 (as of 2/14/25), here’s how the math looks:

- Market Cap: $3.4T

- P/E Ratio: 53

- P/S Ratio: 30

- Gross Margin: 76% (Revenue – COGS)

- Net Margin: 56% (Gross – SG&A)

For its top-tier chips (H100, H200), Nvidia enjoys a mind-blowing 90% gross margin! That means for every $100 in sales, only $10 goes into manufacturing costs.

Over the last 12 months:

- Revenue: $114B

- Net Income: $64B (56% of Revenue)

What Happens If Margins Shrink?

Let’s assume a modest 10% net margin decline.

- New Net Income: $52B

- Keeping the same earnings multiple (P/E of 53), Nvidia’s market cap would fall to $2.7T.

- With 24.5B shares outstanding, that gives a share price of $112 (a 20% decline from the current price of $140).

Now, let’s answer the big question:

Why Would Nvidia’s Margins Shrink?

Nvidia’s biggest customers—AWS, Azure, Google Cloud, Oracle, Meta—are also its biggest threats. These hyperscalers, which account for roughly 40% of Nvidia’s revenue, are all investing in custom AI chips to reduce reliance on Nvidia.

- Google → Trillium

- Meta → Meta Training and Inference Accelerator (MTIA)

- Amazon → Trainium

- Microsoft → Maia

Even if these in-house chips are only 30-50% as efficient as Nvidia’s, Big Tech would save billions by optimizing them for specific workloads.

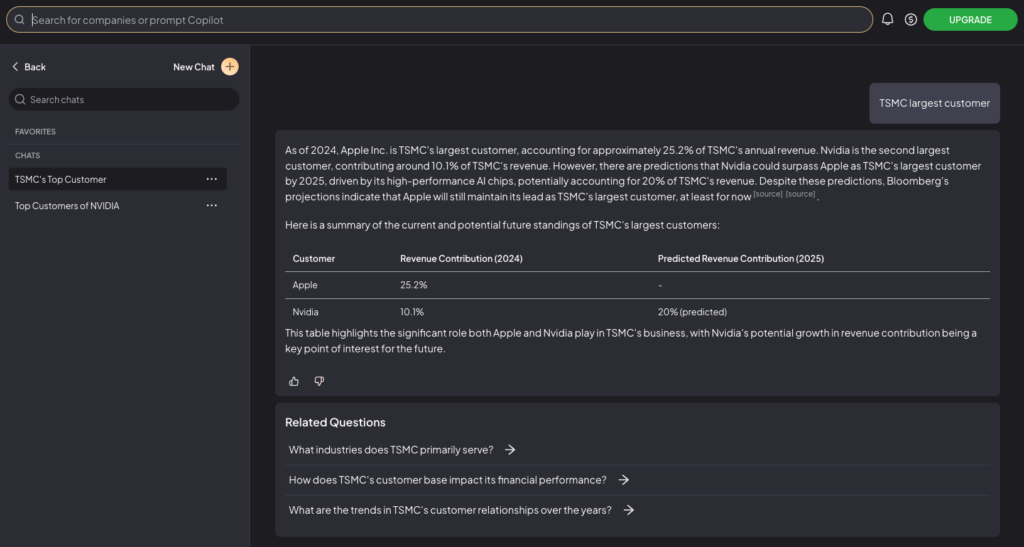

We’ve seen this before. Remember how Apple ditched Intel for its own M1 chips? Today, Apple is TSMC’s largest customer—nearly twice as big as Nvidia!

Another useful analogy to look at here is the DRAM business where Samsung (41%), SK Hynix (34%), and Micron (22%) are the three big players. Micron has a gross margin of 30%, and its stock is as cyclical as it gets depending upon the spending cycles on new data center infrastructure.

Nvidia certainly has a more dominant position than Micron. It clearly has an edge over other competitors in the space such as AMD with its CUDA architecture, which provides a software to efficiently use all the parallel processing power available in the hardware. I expect this gap to close in the next 2-3 years.

In general, for capital expenditure on hardware, the cost is typically amortized over 5-7 years by most companies.

Similar to when you buy a smart phone worth $900, most people expect to use it 3-4 years for an annualized cost of say $300. You only make $900 investment every 3-4 years, so assuming Nvidia revenues will continue growing in a straight line without cyclicality is a hard pill to swallow.

The Bottom Line

Right now, at a P/S ratio of 30, you’re paying a premium that assumes Nvidia will dominate AI hardware without any margin compression.

I don’t buy that assumption.

Nvidia is an incredible company, but even great companies don’t always make great investments!

That’s why—for now—I’m staying on the sidelines.

What’s a better bet you ask? Taiwan Semiconductor Manufacturing Company (TSMC).

No matter what chips will be used in AI, TSMC will still be manufacturing it.

Get freshly brewed hot takes on Product and Investing directly to your inbox!

One response to “Before You Buy the Nvidia Dip, Read This”

Your content has a way of motivating change while offering real-world solutions. It would be intriguing to see you unpack how these ideas might connect with global challenges, such as climate resilience or ethical AI. Your knack for finding patterns is truly remarkable. Thank you for always delivering such impactful content—I’m eagerly anticipating your next piece!