In a market often obsessed with frontrunners, I’ve recently made a contrarian move by initiating a position in Lyft (NASDAQ: LYFT) for my fund. I see it as an easy double in the next 2-3 years.

While most investors have written off Lyft as a perpetual second-place finisher to Uber, I see compelling reasons why this ridesharing platform deserves a closer look—especially with its stock down 82% from its March 2021 pandemic-era highs.

Business Overview

Lyft operates as one of the two major ridesharing platforms in North America, focusing exclusively on the US and Canadian markets. Unlike Uber, which has diversified into food delivery (Uber Eats) and logistics (Uber Freight), Lyft maintains a laser focus on its core ridesharing business.

Key 2024 Performance Metrics:

- Active Riders: 44 million

- Active Drivers: 1.4 million

- Total Rides: 828 million (~2 million rides per day)

- Total Revenue: $5.8 billion (up 31% YoY)

- Net Income: $23 million (compared to a $340 million loss in 2023)

While Uber dominates with approximately 74% market share in the US compared to Lyft’s 24%, there’s more to this story than meets the eye. Let’s explore why I believe Lyft represents a compelling investment opportunity right now.

7 Reasons to Consider Lyft as an Investment

1. Ridesharing Is Not a Winner-Takes-All Market

A critical distinction in platform businesses is between “Marketplace Assign” and “Marketplace Assist” models:

- Marketplace Assign (like Lyft and Uber) automatically pairs customers with service providers, with customers largely indifferent to which specific provider they receive. As long as a ride arrives within a standard 4-7 minute wait time, most riders don’t show strong preferences.

- Marketplace Assist (like Airbnb) lets users choose from multiple service providers based on specific preferences, making these platforms more susceptible to winner-takes-all dynamics.

Ridesharing is inherently hyperlocal—a San Francisco resident primarily cares about service availability in San Francisco, not in Tokyo or London. This hyperlocal nature explains why Uber struggled against local champions like Ola in India, Didi in China, and Grab in Southeast Asia, ultimately leading to market exits or competitor investments. On the contrary, Airbnb didn’t face much resistance because it is a global business from the start since most people are looking for stays outside of their home city.

The localized nature of ridesharing creates a natural floor that prevents bankruptcy or permanent capital loss for investors. Lyft isn’t going away simply because Uber dominates globally. Instead, Lyft is positioned to grow alongside the expanding ridesharing market.

2. Addressing the Elephant in the Room – the AV Threat

Autonomous vehicles (AVs) undoubtedly represent the future of transportation, and experiencing Waymo’s driverless service feels nothing short of magical. However, several practical challenges will likely prevent a 100% autonomous future for at least another decade:

- AV Economics: The customized Jaguar F-Pace vehicles in Waymo’s San Francisco fleet cost an estimated $150,000-$200,000 each—4-5 times more than an average car. Financing these vehicles at scale presents a significant hurdle.

- Fleet Management Complexity: Even autonomous vehicles require cleaning, charging, servicing, and parking during downtime. Operational efficiency in fleet management is where incumbents like Lyft can provide tremendous value—and Lyft’s Flexdrive subsidiary is already working in this space.

- Market Expansion: Autonomous vehicles are expanding the total addressable market beyond traditional ridesharing users. For instance, young children and teenagers—previously unable to use ridesharing due to safety concerns—are now riding in Waymos independently.

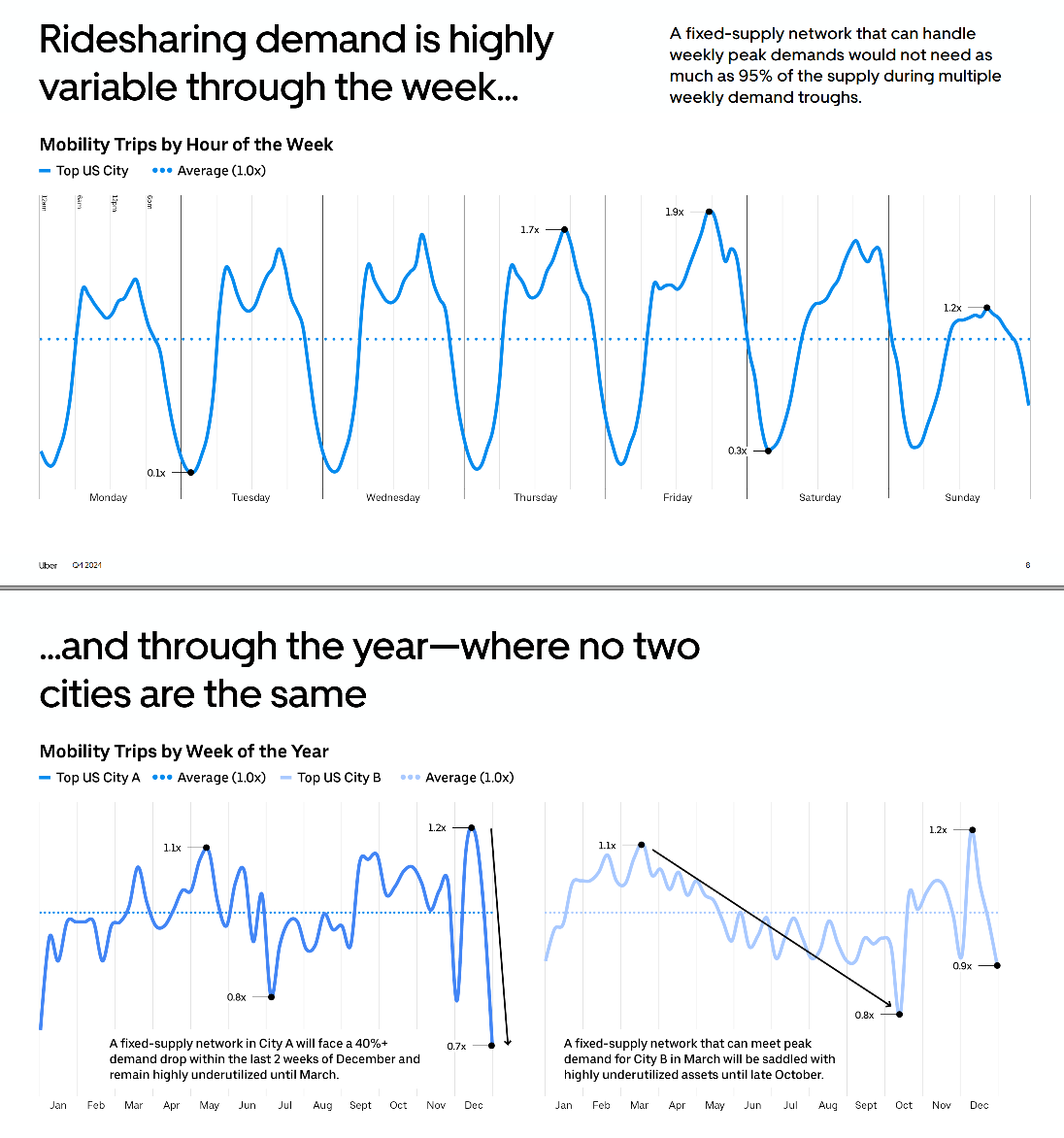

- Demand Variability: Managing peak and off-peak demand remains challenging. The optimal solution likely involves a hybrid network of autonomous and human-operated vehicles, allowing for the most cost-efficient fleet management.

Here’s an interesting analysis on AVs shared by Uber to investors in their Q4 2024 earnings call that resonated with me.

3. Compelling Valuation

The most persuasive argument for investing in Lyft is its current valuation:

- Market Cap: $5 billion

- Cash: $2 billion

- Net Debt: $0.75 billion

- Enterprise Value: $3.75 billion

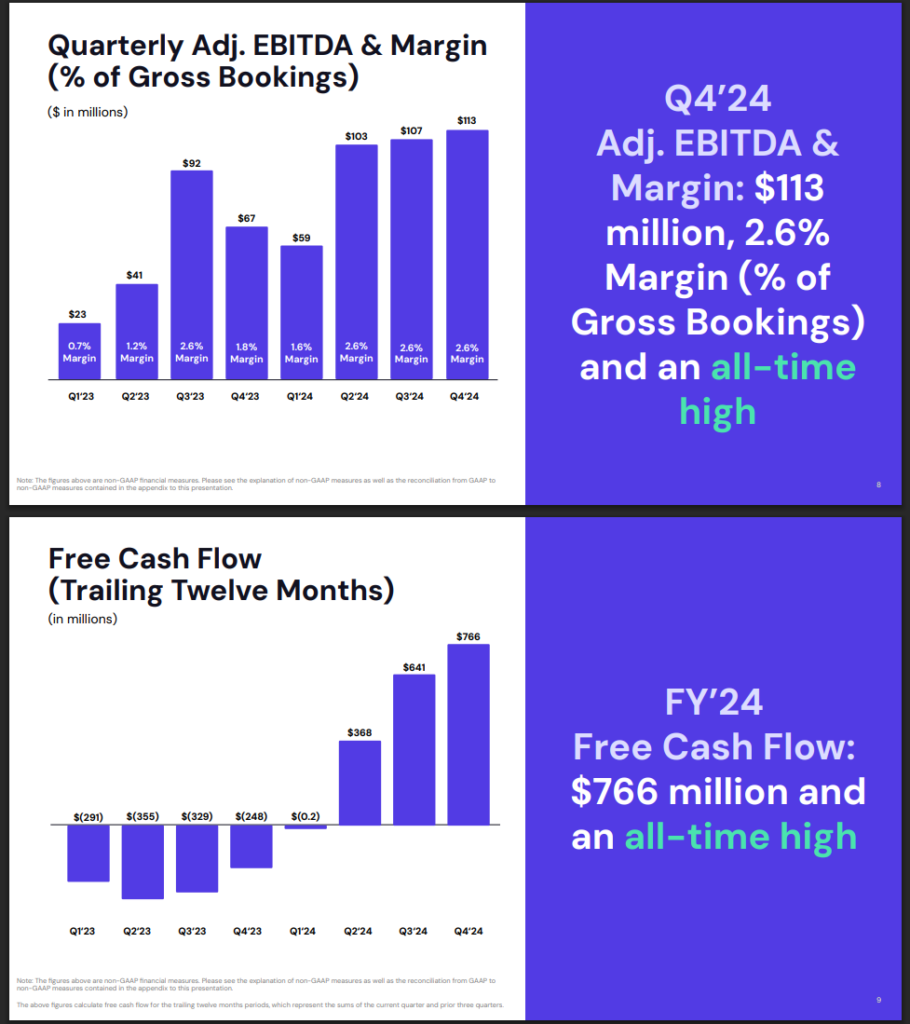

The company recently achieved profitability, reporting net income of $62 million in Q4 2024 and adjusted EBITDA of $113 million and a free cash flow (operating income – cap ex) of $766 million.

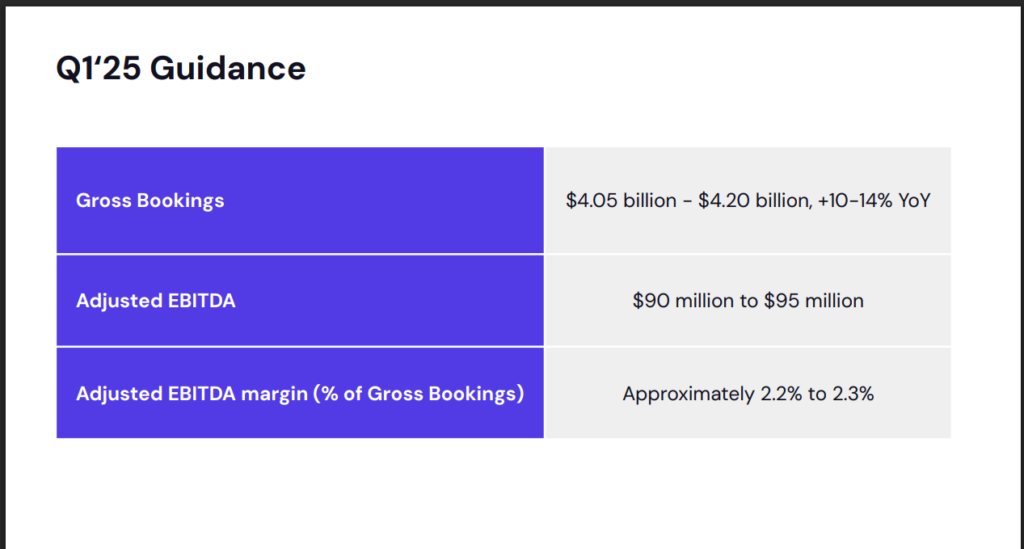

For Q1 2025, management has guided for low double-digit growth in gross bookings (+10-14%) and EBITDA margins of 2.3%.

Assuming 14% bookings growth, we can project quarterly gross bookings of $4.2 billion, or approximately $17 billion annually. At 2.3% EBITDA margins, this suggests around $400 million in 2025 EBITDA.

This gives us an EV/EBITDA multiple of 9, compared to Uber’s forward EV/EBITDA of approximately 18.

Alternatively, I estimate Lyft could generate $300-350 million in net income in the next couple of years. With the current S&P 500 multiple of 25 that gives me a valuation of $7.5B on the conservative side – a 50% return from current valuation (excluding any share buyback effect).

4. Emerging Media Business

The average Lyft ride lasts 17 minutes, during which riders check their phones roughly 7 times. This presents a substantial untapped opportunity for advertising revenue.

Over 40% of Lyft rides start or end in low-income areas, offering advertisers access to otherwise difficult-to-reach demographics. If Lyft can build an advertising network targeting these neighborhoods and use the revenue to subsidize rides, it creates value for both the company and its users.

Uber has already demonstrated the viability of this model, building a $1 billion advertising business. Lyft’s media business is projected to grow 100% year-over-year, reaching an expected annual revenue run rate of $100 million in 2025. Once the initial engineering infrastructure is in place, these revenues should flow directly to the bottom line.

5. Product Innovation in a Commodity Business

While innovation in ridesharing is challenging due to its commodity nature, Lyft has developed several features targeting specific customer segments:

- Women+ Connect: Automatically pairs female riders with nearby female drivers, addressing safety concerns following negative publicity (src1, src2) around women’s safety in ridesharing.

- Lyft Silver: Features designed specifically for elderly passengers, similar to Uber’s Caregiver service.

- Price Lock: Allows daily commuters to avoid surge pricing with a small $2.99 monthly fee.

- Earnings Commitment: Guarantees drivers receive at least 70% of passenger fares.

- Pay with Points with Bilt: Partnership allowing users to pay for rides using points earned from the Bilt Mastercard, which uniquely offers rewards on rent payments—targeting urban professionals who prefer not to own cars.

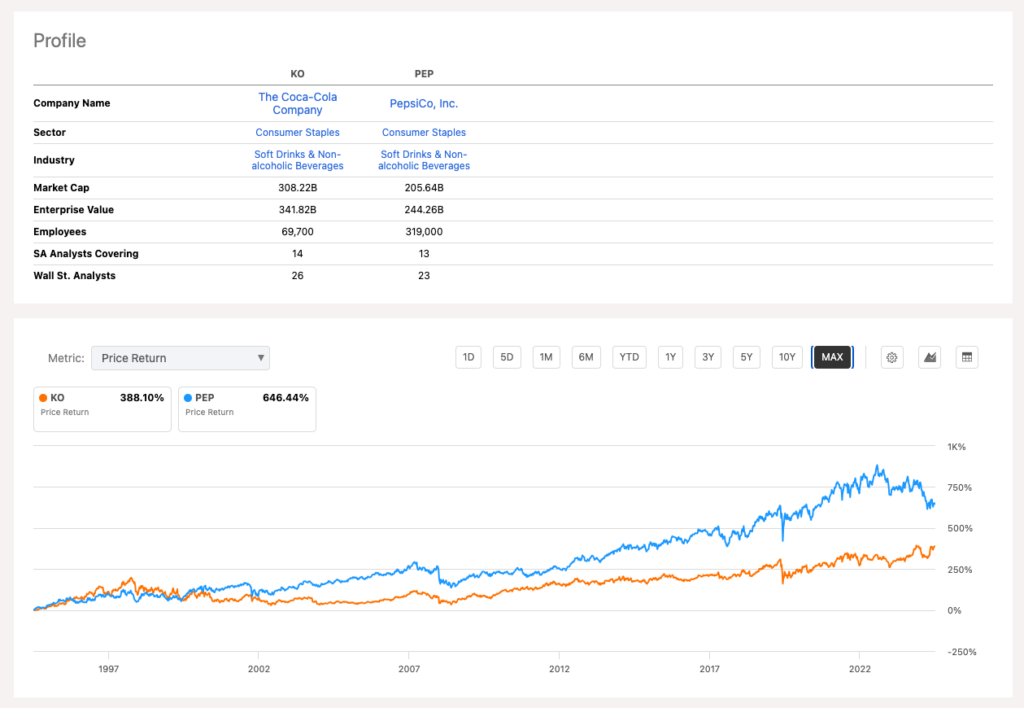

I’d say though most of these features can be easily copied by other competitors. This reminds me of the duopoly between Coco Cola (NYSE:KO) and Pepsi (Nasdaq: PEP). While Coke is still the dominant player in the beverage industry, Pepsi did a great job at diversifying its business in other packaged food items. Over the long period, both Coke and Pepsi shareholders have done well.

6. Shareholder-Friendly Management

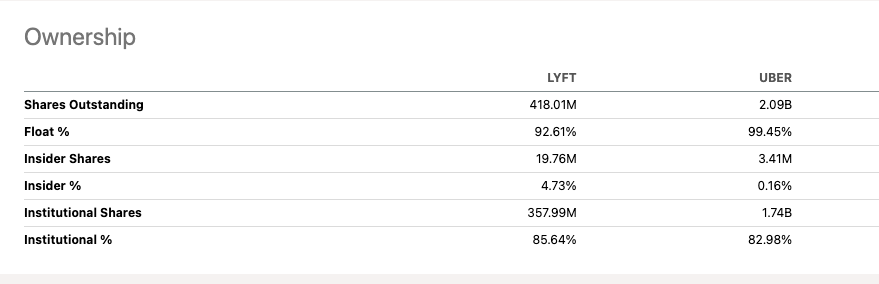

Lyft’s insider ownership structure is encouraging. CEO David Risher owns approximately 1.5% of the company, with total insider ownership around 5%.

Management recently announced a $500 million share repurchase program, signaling their commitment to addressing the value gap. Additionally, activist investor Engine Capital has taken a 1% stake in the company to help drive shareholder value.

7. M&A Optionality

Another great thing about Lyft is the number of M&A possibilities. Lyft has great assets that can be valuable to a lot of different players in the logistics and transportation space.

- Amazon: Following its investment in Zoox, Amazon could see value in acquiring Lyft to enhance its logistics network and manage variable capacity in its delivery operations (source: YFinance, The Information)

- Waymo: Although Waymo currently has a multi-year strategic partnership with Uber for AV deployment in Austin and Atlanta, acquiring Lyft would provide valuable insights into user behavior and expand its market presence. Back in 2017, Capital G – the venture arm of Alphabet – already invested a $1 Billion in Lyft at a valuation of $11 Billion, so an all out acquisition at less than half that valuation is very much a possibility.

- DoorDash: With ambitions to become a logistics super-app competing with Amazon and Instacart, DoorDash could leverage Lyft’s driver network, particularly during off-peak hours when ridesharing volume decreases.

Final Thoughts

While Lyft faces significant challenges—including intense competition from Uber and the looming threat of autonomous vehicles—its current valuation fails to reflect its improving fundamentals, emerging growth opportunities, and strategic optionality.

Bottom Line: Lyft isn’t going away—and at this valuation, the risk/reward looks compelling. I believe patient shareholders will be rewarded.

Disclosure: I am long LYFT. This is not financial advice. Do your own research before investing.

Get freshly brewed hot takes on Product and Investing directly to your inbox!

Leave a Reply